A look at how innovation is modernizing wealth management in the United States

Background

For much of the first half of the 20th century, financial advice was considered something only relevant to the wealthiest individuals in the United States. Advisors would cater to the one percent of the one percent along with institutional investors, with an emphasis on accumulating AUM and building relationships that would span generations. The momentum for the shift towards the broader adoption of financial advice began in the mid-20th century as holistic financial planning started to take shape in the late 1960s and early 1970s, culminating in the creation of the College for Financial Planning in 1972 and the Certified Financial Planner (CFP) in 1973.1 As the 21st century neared, the rise of the internet and democratized access to information and tools for investors and advisors began to shape the modern day of wealth management. For advisors, we saw the founding of Financial Engines in the 1990s, which provided automated retirement planning advice to 401(k) sponsors and plan participants. While consumers were struggling with complex investing decisions, particularly 401ks, advisors were able to gain access to sophisticated investment modeling and financial planning technology previously only utilized by institutional investors. Furthermore, it was in the 1990s when online trading became popular for individuals. While E-trade (founded in 1982) was not necessarily the first online trading platform, it quickly gained momentum. In addition to offering an innovative discount online trading platform, the company introduced flat-rate trading fees and free investment information online, making stock trading more accessible and affordable for the average person.234

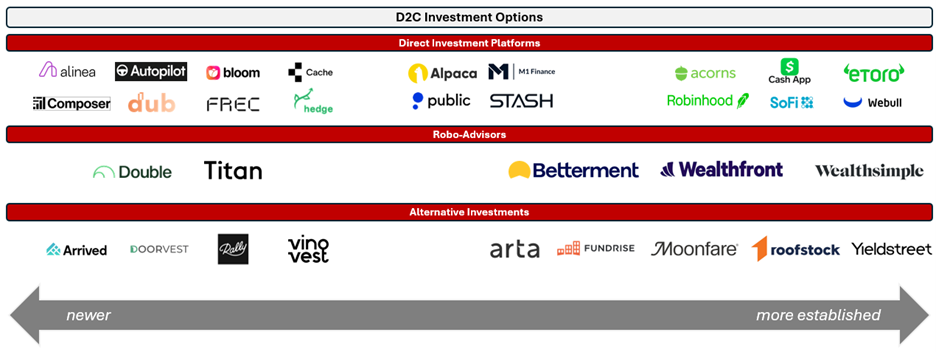

As consumer-led investing and complex decision-making led by data-driven analytics propagated, the Global Financial Crisis of 2008 struck, exposing the risky operations led by leading financial institutions. As the global financial market was flipped on its head, consumers demanded transparency and clarity in investment approaches leading to the emergence of the robo-advisor. Both founded in 2008, Betterment and Wealthfront led the charge with the goal of automating investment management based on algorithms, lowering the cost of financial advisory, increasing accessibility, and providing transparency.5 While robo-advisors gained relevance, the waves of the 2008 financial crisis continued to drive consumer demands. Like the initial idea for robo-advisors, Robinhood’s goal was to make investing cheaper, easier, and even more convenient for consumers, using a mobile-first design. Robinhood was a pioneer because it delivered on the promise that “anyone” could invest with no minimum-based investments.6 Around the same time, Acorns and Stash emerged to offer passive investing (buying and holding a diversified portfolio, often through index funds, to match the market’s performance) and micro-investing (regularly investing small amounts of money into the markets) for consumers, another way to enable entry into the financial markets not previously as easily attained. Since then, we’ve seen many more entrants give consumers ways to take control of investing, offering innovative ways to improve one’s financial status. The rapid advancement of technology, restrictive advisor fee structures, and explosion of consumer demand for transparency led to a massive pool of optionality for consumers to test the waters in investing for the short and long term.

Still though, these platforms have not been seen as replacements for financial advisors, but rather have challenged the potential wallet share an advisor may have for individuals and have encroached on the early attention of the next generation of investors. While direct-to-consumer platforms have been experiencing rapid growth, driven by evolving preferences and technological innovation, financial advisors have remained critical. They deliver personalized guidance tailored to individual risk appetite, specific short-term and long-term goals, and complex financial needs that automated tools cannot fully replicate.7 Furthermore, because of the market’s extremely dynamic nature, financial management goes well beyond just asset allocation. It involves a wide range of decisions along the way, such as estate, tax, and retirement planning, among many others. Lastly, financial advisors offer invaluable solutions for time and resource efficiency, given research, ongoing management, and administrative tasks that come with these ever-evolving events.

Advisor landscape

This paper focuses specifically on the current American advisor landscape and its market dynamics, rather than the global context, given the inherent differences between regions. Key factors driving this divergence lie in the varying regulatory frameworks and consumer investment behaviors that shape each market. For instance, in the United Kingdom, the FCA (Financial Conduct Authority), the regulator overseeing the financial services industry, requires prospective fund managers to undergo a lengthy approval process. This process involves applications, and multiple interview rounds, often taking between 6 to 18 months to complete, making it considerably more rigorous than the in the U.S. As a result, financial advisory services in the UK tend to be concentrated within banks and large institutions. By contrast, the U.S. market offers far greater flexibility and optionality for both advisors and investors. In addition, investor psychology further reinforces these differences. European investors are generally more risk-averse, preferring stability over new products. Conversely, American investors are more inclined to pursue innovative, and at times riskier, investment opportunities. This appetite for greater upside creates a more diverse and expansive array of financial products and services in the U.S. compared to Europe.

To expand on the optionality in the United States, there is a wide range of firms that typically come with a pitch, approach, and target demographic. In addition, these firms also have their own propensity and ability to quickly adopt new technologies. Categories of firms include wirehouses, national broker-dealers, regional broker-dealers, Registered Investment Advisors (RIAs), and more recent entrants, tech-enabled RIAs.

Wirehouses, managing the most AUM of the group, are not considered strong candidates for mass tech adoption. Technology used is typically developed in-house or pieced together through strenuous onboarding processes, and primary customers targeted include ultra-high net worth individuals and institutions who typically prefer fully managed experiences. For both national and regional broker dealers, advisors often have the choice of utilizing different technologies across the stack, although tech must be approved by compliance, security, and IT to ensure reliability, safety, and value within the context of the firm. Next, RIAs are where we see the most seamless opportunity for technological adoption, given the typical smaller nature of firms, leading to more agility and flexibility. Advisors commonly have more independence and accumulate or acquire books of business over time that are tailored to one’s skillset and background. Lastly, we more recently have seen modern tech-enabled RIAs enter the space, recognizing the slow-moving nature of the industry and advisor’s desire for modern tech. These organizations are often the most nimble, either adopting or building solutions on the fly.

Before exploring technological innovation opportunities for advisors, it’s helpful to outline a key aspect of the investor landscape that is driving much of the movement in the market. This context highlights some key trends in asset and wealth accumulation, as well as evolving investor expectations, which are driving advisors to adapt and innovate. The phenomenon being referred to is the highly publicized impending “Great Wealth Transfer.” As of today, there are over 76 million baby boomers living in the United States. Baby Boomers collectively hold an astonishing $79 trillion of assets, representing over half of all US wealth. With baby boomers today ranging from 61 to 79, we can expect that over the next 15-30 years, a large majority of that wealth will be transferred, often ending up in the hands of a younger generation. But wouldn’t the offspring of wealthy baby boomers always use their parents’ advisors, you may ask? It turns out that only 41% of those under 30 do so, with the number dropping to just 19% when you include older generations.8 If that wasn’t enough to convince advisors to begin modernizing and emphasizing relationships with younger individuals, it was reported that American households below the age of 40 saw their average net worth grow by 49%, adjusted for inflation, from late 2019 to late 2023 reaching $259,000. More specifically, millennials alone saw their wealth double during this period. Comparatively, Americans aged 40 to 54 (mostly Gen X) experienced a 7% drop in wealth, while those aged 55 to 69 (mainly baby boomers) saw their wealth increase by just 4%.9

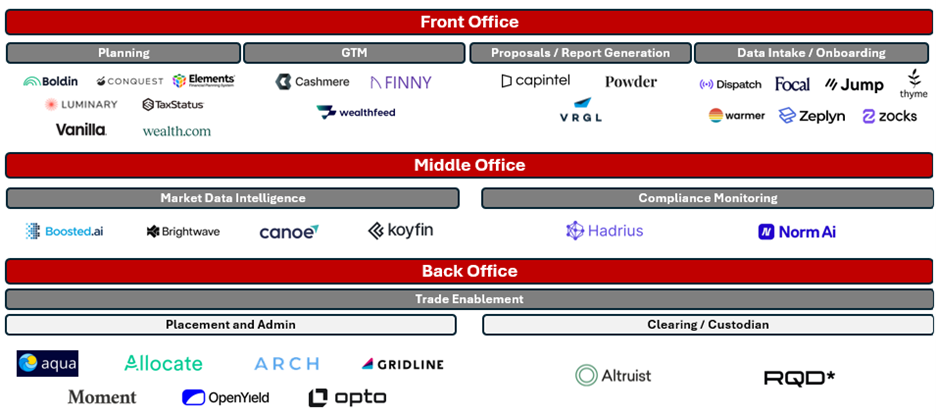

Technology stack

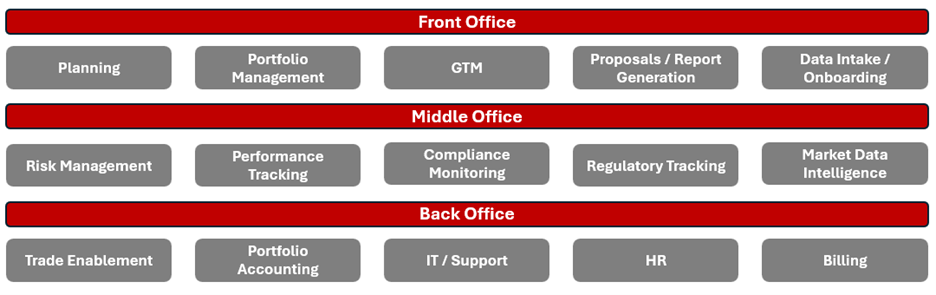

To identify opportunities for modern technology in wealth advisory, it’s helpful to map out all the tools and services that support a firm’s operations. Like other enterprise software sectors, wealth management technology is typically organized into three main areas: front office, middle office, and back office.

Within the technology stack, we’ve seen areas of heightened innovation, investment, and rapid growth. What underpins much of this growth is the ability to drive efficiency through automation, enabling advisors to serve more clients, and deliver more personalized insights and solutions for clients. In fact, the two are connected, given how we see each reinforcing the value of the other in modern advisor operations. In practice, automation streamlines repetitive and manual tasks, reduces errors, and optimizes workflows, allowing firms and advisors to take on more clients with fewer resources and less capacity. Furthermore, automation, especially when powered by AI, can leverage vast amounts of unique customer data in real-time to uncover individual preferences, behaviors, and needs, answer specific questions, create personalized products, and solve unique problems.

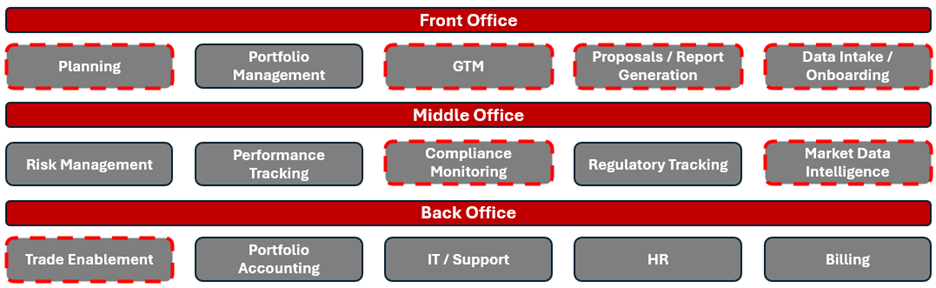

Areas to highlight where we’ve increasingly seen activity are the following:

So, if multiple large players already exist to serve wealth firms and financial advisors, such as Envestnet, SEI Investments, AssetMark, and Orion, among others, why is there so much activity in the space? The first reason is that advisors have not been shy to express the shortcomings of their technology. Led by the rapid development of AI, there is a clear awareness from advisors that platforms and tools that were leaned on 5 years ago, are likely far behind in their ability to provide outsized value in terms of automation, efficiency, and personalization. In Advisor360’s latest report, sixty-five percent of respondents cited that their technology setup needs to be improved, citing bad data and lack of automation as the biggest problems. Furthermore, 92% of advisors would leave their firms over bad technology, and a reported 44% said they already have.10 Technology enables advisors to efficiently serve a larger number of clients, including those with fewer assets, through the automation of routine tasks and powerful client deliverables. This allows advisors to maintain their focus on complex, high-net-worth clients while also building relationships with emerging investors who may become more valuable clients as their assets grow or, acquiring new clients looking for a better experience.

Areas of interest

Front Office

Planning

New entrants in financial planning are emerging to meet the growing demand for hyper-personalized insights tailored to a wide range of client needs. Key areas addressed by these solutions include cash flow management, tax optimization, retirement planning, estate planning, education funding, and philanthropic giving. By delivering highly customized guidance in each of these domains, often through scenario modeling, interactive visualizations, dynamic dashboards, and proactive, automated insights, these platforms are enhancing advisor-client engagement. The main result is improved client retention, as advisors can present complex information in formats that are both accessible and actionable.

GTM

GTM tools leveraging AI have shown the ability to identify, score, and prioritize leads with far greater accuracy. AI analyzes vast datasets from private and public sources such as CRM, social media, and public records. The goal is to pinpoint prospects most likely to convert, saving advisors time and boosting efficiency. The next step observed is often personalized and automated outreach to drive high-quality candidates into an advisor’s sales funnel, improving prospect pools and conversion rates.

Proposals and Reports Generation

Proposal generation has become a vital part of an advisor’s toolset, as it enables the inclusion of powerful, personalized information that drive conversion. Given the information that goes into a proposal, such as risk tolerance, financial standing, short and long-term goals, market information, and optionality of investments, automating such deliverables can lead to extreme time saving and clear signaling of an advisor’s knowledge and capabilities. Furthermore, ongoing report generation is revolutionizing how financial advisors communicate with clients by transforming complex, text-heavy documents into clear, easily digestible insights. These advanced tools automatically distill large volumes of financial and performance data and analysis into concise summaries, interactive visualizations, and actionable highlights tailored to each client’s needs.

Data Intake / Onboarding

Similar to proposal generation, we’ve seen a rise of companies looking to automate the tedious task of client data and information intake. Modern approaches like having AI integrate with different file storage/sharing resources as well as joining meetings to create actionable tasks, notes, and compliance records, save advisors countless hours. It’s important to note that these platforms must emphasize privacy and data security, given the highly sensitive nature of information shared with advisors.

Middle Office

Compliance Monitoring

Regarding compliance monitoring for wealth firms and financial advisors, there is a wide variety of technology and resources to serve the different profiles of firms. Compliance resources are vital for financial advisors to protect clients, manage risks, and maintain trust in a highly regulated industry. Their diversity reflects the complexity of financial regulations, the evolving nature of the industry, and the varied needs of advisors and their clients.

Market Data Management

Modern market data management tools are transforming how financial advisors operate by providing seamless access to both established and emerging data feeds. These platforms empower advisors with actionable market intelligence, advanced analytics, and comprehensive research capabilities, as well as robust peer benchmarking and operational support. With AI-powered insights delivered from real-time data, advisors can quickly analyze trends driving educated decisions. Additionally, these tools are designed for easy integration, enabling advisors to incorporate data into other platforms and workflows for deeper analysis and more effective client service.

Backoffice

Trade Enablement

For broader trade enablement, both Alternative Investment and Fixed-income markets have traditionally posed challenges for advisors, with high minimums, complex administrative requirements, and operational complexity making efficient access difficult. Modern platforms address these barriers by incorporating necessary trading functionalities like pooling of capital, trading protocols, and access to liquidity sources. In addition, by embedding advanced analytics and workflow enhancements, advisors can seamlessly integrate fixed income and alternatives into broader portfolios and streamline back-office operations. This not only expands access but also improves efficiency and portfolio management for a wider range of clients. Separately, reliance on outdated, fragmented systems has led to an opportunity for next-generation clearing platforms to offer features such as faster account opening, real-time reporting, and billing automation to drive innovation and efficiency.

Market map

Broader platform approaches

We have also seen companies launch with broader platform solutions or expand over time to challenge incumbents in the space. When you think of the center of the wealth management technology landscape, you often think of platforms aiming to deliver a Turnkey Asset Management Platform (TAMP), which streamlines and automates a broad array of portfolio management needs. TAMPs commonly handle investment research, portfolio construction, rebalancing, asset allocation, trading, reconciliation, and performance reporting, enabling advisors to dedicate more time to impactful business activities rather than administrative and operational responsibilities.11 For these platforms, packaging the right combination of solutions is key, along with broad and deep integrations to cover multiple functions and roles across organizations. Furthermore, we have also seen more modular technology-driven entrants look to offer purpose-built products across both advisor and client needs to limit the fragmented nature of the financial advisor toolset.

Conclusion

As discussed above, while some early-stage companies enter the market with a broad platform approach, most initially focus on a specific product designed to address a well-defined pain point for financial advisors. As investors, a common challenge arises when assessing the total addressable market or market opportunity for these narrower solutions. In 2024, there were just 15,87012 registered investment advisors in the US, therefore requiring an average annual contract value above $60,000 needed to support a $1 billion-plus annual market opportunity. Although large contracts with Wirehouses and Broker-Dealers are possible, these deals are relatively rare, and require strenuous due diligence and onboarding processes. Therefore, there are two primary strategic paths forward, which are often done concurrently. First, you can demonstrate how technology solutions for financial advisors deliver substantial value by either increasing revenue or reducing operational costs. Second, you can focus on developing additional products to broaden the value proposition and expand market potential.

In the end, what underpins much of AVP’s belief in the future of wealth technology, is that individuals still believe in having a strong, long-term relationship with a financial advisor. While we have certainly seen a push from countless new direct-to-consumer investment platforms, personalized, objective guidance to help navigate complex decisions and achieve tailored financial goals will continue to be maximized by financial advisors. Furthermore, the financial advisory industry faces significant opportunities to improve through better technology, with AI driving much of this innovation. While some firms are more eager and able to embrace new tools, leveraging technology is especially promising for reaching and selling to the next generation of clients as well as retaining high-value clients who demand a better experience.

Bibliography

[1] “Financial Planning: Detailed History, 7 Steps & Benefits.” 49th Parallel Wealth, 24 May 2025, 49thparallelwealthmanagement.com/the-evolution-of-financial-planning-from-early-firms-to-a-thriving-profession/.

[2] Rusoff, Jane Wollman. “William Sharpe: There Is No Retirement ‘Number.’” Thinkadvisor.Com, ThinkAdvisor, 20 Sept. 2021, www.thinkadvisor.com/2021/09/20/william-sharpe-there-is-no-retirement-number/.

[3] Wu, J., Siegel, M., & Manion, J. (1999, June). Online trading: An Internet revolution (Sloan Working Paper No. 4104, CISL WP #00-02). MIT Sloan School of Management.

[4] Team, Windmill Editorial. “All about Wealthtech: Past, Present, and Future.” Windmill, 2 Dec. 2024, windmill.digital/all-about-wealthtech-past-present-and-future/#:~:text=Stage%201:%20Origin%20of%20Wealthtech,been%20around%20since%20the%20’90s.

[5] Filipsson, Fredrik. “The History of Robo-Advisors and Automated Investing.” Redress Compliance – Just Another WordPress Site, 27 July 2024, redresscompliance.com/the-history-of-robo-advisors-and-automated-investing/.

[6] Svensson, Philip. “Robinhood: Revolutionizing Retail Investing.” Quartr, 7 Nov. 2024, quartr.com/insights/company-research/robinhood-revolutionizing-retail-investing.

[7] “The Changing Role of Financial Advisors in the Age of Digital Investing.” Financial and Business News | Finance Magnates, 27 Apr. 2023, www.financemagnates.com/fintech/investing/the-changing-role-of-financial-advisors-in-the-age-of-digital-investing/.

[8] “Cerulli Finds Just 19% of Investors Use Their…” Cerulli Associates, 14 Nov. 2023, www.cerulli.com/press-releases/cerulli-finds-just-19-of-investors-use-their-parents-advisor.

[9] Weller, Christian E. “Wealth of Younger Americans Is Historically High.” Center for American Progress, 4 Apr. 2024, www.americanprogress.org/article/wealth-of-younger-americans-is-historically-high/.

[10] Schwantz, Jeff. Advisor 360, 2024, 2024 Connected Wealth Report.

[11] “What Is a Turnkey Asset Management Platform?” GeoWealth, 19 Feb. 2025, geowealth.com/what-is-a-tamp-turnkey-asset-management-platform/.

[12] “Industry Statistics.” Investment Adviser Association, 31 May 2025, www.investmentadviser.org/industry-snapshots/.