Arthur Brasseur

Senior Associate

Isabel Young

Senior Associate

Augustin Collot

Analyst

In our previous blog, we unpacked the global race for robotics dominance and the technologies driving it. Now, we turn to where the real action lies: the sectors primed for transformation, the investor playbook, and what’s still holding robotics back.

In robotics, form and function are inherently linked – much like in software UI design, where interfaces are tailored to specific use cases. As a result, distinct types of robots have emerged to meet the needs of different applications: robotic arms dominate in manufacturing automation, cobots are built to work safely alongside humans, AMRs are optimized for logistics, quadrupeds for inspection, and service robots handle applications in domestic or retail settings. At the other end of the spectrum, humanoid robots are designed to mimic the form and dexterity of the human body, aiming to operate in environments originally built for people without requiring major adaptation. Companies like Tesla (Optimus), Sanctuary AI, Agility Robotics, and Figure are betting on the humanoid form factor to unlock general-purpose robotics. While this approach is promising, it remains technologically early and capital intensive.

In contrast, verticalized robots seem more pragmatic and built for clearly defined, high-ROI use cases in structured environments. These robots trade general-purpose flexibility for performance, speed of deployment, and return on investment. They are already demonstrating traction in sectors like medical, manufacturing, logistics, and construction.

That said, humanoid robots may still play an important role in general-purpose, unstructured environments such as homes or office buildings – where flexibility or dexterity matter more than efficiency. Over time, a few standard form factors may emerge just as the chatbot interface became the default UI for consumer AI.

AVP believes that certain historically labor-intensive verticals are particularly well-suited for robotics. By taking a vertical-specific approach, robotics companies can develop deep expertise within a segment and build a competitive moat through data advantages or by solving unique, industry-specific problems. Below are some of the key verticals that are ripe for disruption:

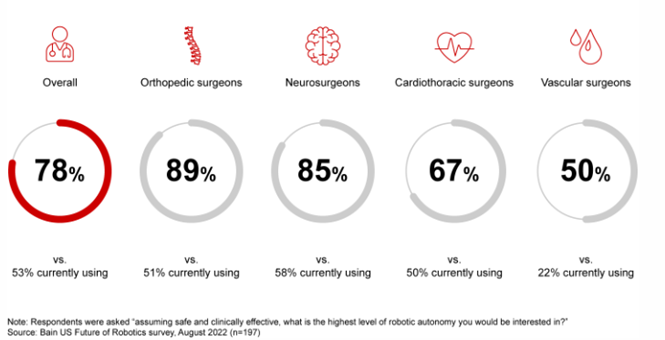

- Robotics is transforming healthcare, where precision is crucial, and errors can be life-threatening. While used across many areas, surgery stands out for its clear benefits – offering greater consistency, fewer errors, and improved patient outcomes. The surgical robotics market has expanded rapidly, growing from approximately $800m in 2015 to around $3.5bn today, with 78% of surgeons interested in adopting robotic systems. The da Vinci System, the most widely used multiport robotic surgery platform, has been used in more than 12m procedures globally. Public companies like Vicarious Surgical are pushing the frontier further, using a single small incision to insert a camera and two robotic instruments. AI is now accelerating the next phase of development. A recent Johns Hopkins University study showed that a robot trained through imitation learning achieved accuracy comparable to that of experienced surgeons. When applied, this approach eliminates the need for manual programming and allows surgical robots to learn new procedures within days. This advancement is accelerating adoption and building on the clinical benefits already demonstrated.

Percentage of Surgeons Interested in Surgical Robots

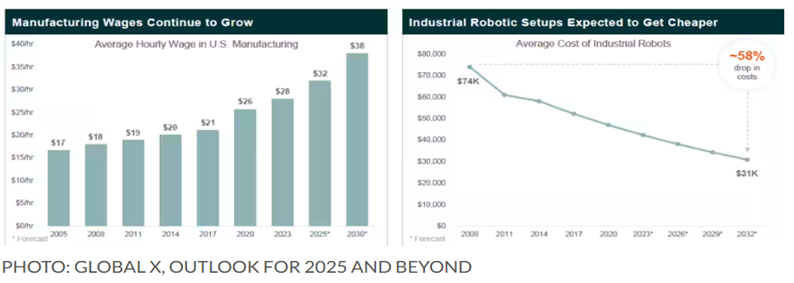

- The manufacturing sector has relied on robots for decades. It was the first industry to adopt them. Today, there are more than 4m industrial robots in use, with the automotive industry leading in adoption. Many tasks done in a factory setting such as pick-and-place and inspection, traditionally done by humans, are increasingly being replaced by robots. Macro trends are driving this shift: nearshoring, an aging workforce, and rising labor costs are pushing manufacturers. Robotics adoption can significantly enhance efficiency, quality, and reduce costs. In fact, wages in manufacturing are expected to grow 125% whereas the average cost of industrial robots is expected to decrease 58% between 2005 and 2030. We are excited about vertically focused companies like (i) Energy Robotics, which are developing a fleet management platform for inspection or (ii) Maven Robotics, which are developing robots for various high-repetition manufacturing tasks. In contrast, humanoid robotic platforms developed by companies like Agility and Figure are designed to serve as flexible, general-purpose workers on the factory floor, offering more horizontal capabilities and may not perform as well on specialized tasks.

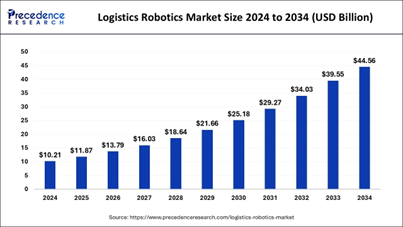

- The logistics and transportation sector presents a significant opportunity for robotics automation. Currently, most warehouses are manually operated with limited automation. Robots can be deployed across various functions, from container loading and unloading to last-mile delivery, especially with recent AV and computer vision advancements. According to a report by ABI Research, last-mile delivery revenue from robotics is expected to grow by +850%, from $70m in 2022 to $670m by 2030, as companies increasingly adopt them as a convenient delivery solution. Industry giants like Amazon and Alibaba have set the bar by investing heavily in robotics. For example, in 2019 Amazon launched Scout, a delivery robot the size of a small cooler that navigates sidewalks. In June 2025, Amazon also announced plans to roll out AI robots capable of completing tasks without human intervention. Other companies are forming partnerships with robotics firms, for instance; Uber Eats plans to deploy 2k Serve Robotics last-mile autonomous delivery robots in the US by the end of 2025. Overall, we expect the logistics landscape to look very different in the coming years.

Source: Logistics Robots Market Size

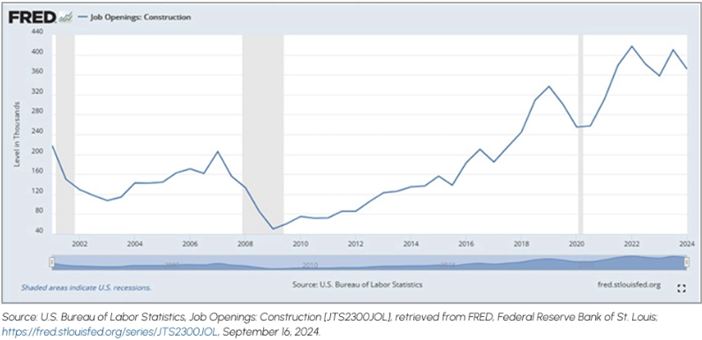

- Construction is emerging as an important area for robotics, offering a safer and more efficient alternative in a traditionally manual and high-risk industry slow to adopt innovation. According to McKinsey, the $12tn global architecture, engineering, and construction (AEC) industry ranks among the least digitized sectors, creating space for disruption. At the same time, the industry faces acute labor shortages – approximately 440k positions remained unfilled in 2023, and the National Center for Construction Education and Research (NCCER) projects that ~41% of the current workforce will retire by 2031. Robotics has the potential to drive meaningful impact across the construction lifecycle from preconstruction to on-site building. For example, Dusty Robotics‘ FieldPrinter autonomously lays out full-scale BIM designs directly onto jobsite floors, helping crews build with greater precision. Meanwhile, Monumental develops mobile construction robots that collaborate with human workers on-site, focusing initially on autonomous bricklaying. While construction has been slow to adopt new technologies, the combination of workforce pressures and automation positions the sector for significant growth in robotics adoption.

This shift across key verticals reveals the growing promise of robotics, evolving from niche automation into a transformative technology category. Several key trends make this sector increasingly appealing to investors:

- Recent breakthroughs in AI, particularly with foundation models, are enabling robots to generalize across tasks, environments, and hardware. This marks a shift from traditional, rule-based automation to flexible and adaptive systems. As a result, robots can operate in semi-structured environments where it was previously too complex.

- The robotics technology stack is becoming increasingly modular and software driven. Startups no longer need to build full-stack solutions from the ground up. Instead, they can focus on specific layers such as fleet orchestration or sim-to-real transfer. This unbundling of the stack has opened a wave of “picks and shovels” opportunities, where infrastructure and developer tools become attractive, standalone investments.

- Business models are evolving as robotics systems become more intelligent and improve over time. What began as simple RaaS models – typically pay-per-task – are now shifting toward SaaS-like, usage-based pricing. These models allow for margin expansion over time as the system learns, delivering compounding value to customers and reinforcing defensibility through network and data effects.

- The geopolitical landscape is also fueling growth. China’s dominance in robotic hardware is prompting Western countries to diversify their supply chains and seek regional alternatives. At the same time, the White House’s immigration and tariff policies are driving strain on the labor market, which robotics can assist with.

Despite the promise, robotics remains a complex domain with several inherent challenges that investors must carefully consider:

- Robotics lags behind language and vision in data scale, with datasets consisting of millions of episodes versus trillions of tokens for LLMs. It limits progress and often requires expensive, task-specific fine-tuning.

- Robotics sits at the intersection of hardware and software. Hardware is expensive and slow to iterate, while the integration of sensing, control systems, and AI algorithms introduces further complexity.

- Robots often come with significant upfront CapEx, remaining higher than equivalent human labor for many customers.

- Regarding GTM, robotics frequently targets industries like logistics, agriculture, or cleaning – sectors with thin margins and slow tech adoption.

- While humanoid robots generate long-term potential, they remain far from being commercially viable today. These systems are still costly to build and train, difficult to deploy in real-world environments, and offer unclear short-term ROI.

- Widespread adoption of robotics could lead to short-term dislocations in the labor market and could disincentivize robotics adoption.

Given the above dynamics, a successful investment strategy in robotics should focus on:

- Startups with a competitive edge in data have a significant advantage in robotics, where access to high-quality, task-relevant data is a major barrier to entry.

- Verticalized robotics targeting repeatable, high-frequency tasks in structured or semi-structured environments tend to benefit from faster GTM, quicker value delivery, and greater capital efficiency. Starting by solving one specific problem extremely well and focusing efforts on a clearly defined use case before expanding can ensure the solution drives real ROI.

- Middleware and developer tools that unbundle the stack, such as fleet orchestration, OS, data collection, training tools, and vision algorithms.

- As regulation increases, opportunities will emerge around cybersecurity, data privacy, and compliance standards (e.g., ISO 25785-1, NIS2). The need for robust security will grow as robots proliferate across homes or hospitals.

- Companies that treat hardware as a delivery layer and focus on software may offer better margins, faster iteration, and higher defensibility.

Alongside these promising areas, certain segments still present significant challenges and should be approached with caution:

- General-purpose humanoids (short to mid-term) which are exciting with long-term potential but not yet commercially viable at scale.

- Full-stack robotics startups try to build everything in-house – capital intensive and slow to iterate.

- Startups that depend on third-party hardware providers face several structural risks. This dependency can slow development cycles, limit access to low-level sensor data, and create friction around integration. It also introduces scalability challenges, as updates or changes on the hardware side can disrupt software performance and roadmap alignment, and long-term strategic vulnerability.

- Robots that lack learning capabilities or adaptability. We believe that long-term winners will be those whose systems improve autonomy over time.

Conclusion

To conclude, what once felt like science fiction is now edging into reality. Westworld painted a world where robots seamlessly integrated into human environments – intelligent, adaptive, and often indistinguishable from us. While we’re still far from that dystopian vision, robotics is definitely entering a new era.

Today, humanoid platforms continue to inspire and advance rapidly, even if their large-scale deployment remains on a longer-term horizon. In parallel, more narrowly focused vertically integrated systems are already beginning to demonstrate value. From factory floors and hospitals to warehouses and construction sites, robots are not just automating repetitive tasks – they are reshaping entire workflows, enhancing precision, and addressing critical labor shortages.

This transformation is fueled by a convergence of breakthroughs: foundation models that enable generalization across tasks, edge AI that unlocks real-time autonomy, and increasingly modular software infrastructure. Paired with falling hardware costs and rising enterprise demand, these advances are making robotics more accessible, scalable, and commercially viable than ever before.

At AVP, we are especially focused on software-first, vertically integrated robotics startups with clear ROI, defensible data advantages, and focused GTM strategies. We also believe that infrastructure layers – training platforms, operating systems, and fleet orchestration tools – represent critical leverage points in the evolving robotics stack.

For investors, this is a defining moment, and the shift from prototype to real-world deployment is underway.