Constance Bielle

Associate

Augustin Collot

Analyst

When Luca Pacioli published Summa de Arithmetica in 1494, he codified double-entry bookkeeping, giving merchants a framework to view business as an integrated system rather than a series of transactions. That foundation endured for centuries. Today, accounting faces a similar inflection point: artificial intelligence promises not just to automate tasks, but to redefine the discipline itself.

Accounting’s many subspecialties – from bookkeeping and payroll to tax, audit, and advisory – share one common thread: they’re labour-intensive and rely on manual work – an ideal environment for automation to take root. Moreover, they need accuracy and efficiency. AI is now delivering both. New technologies like GenAI, OCR, IDP, and smart agents are taking over repetitive tasks such as data extraction, reconciliation, and invoice processing, reducing errors and freeing professionals to focus on higher-value analysis and judgment.

Yet the true power of AI lies beyond automation. Predictive analytics sharpen forecasts, AI audit tools can test entire data sets in seconds, and anomaly detection systems flag risks before they escalate. Together, these capabilities enable the long-envisioned goal of continuous closing – a state where financial data is updated, validated, and analysed in real time. Instead of waiting weeks for period-end reconciliations, organizations can maintain a live, always-accurate view of performance, turning accounting from a backward-looking process into a forward-looking intelligence system.

But innovation comes with challenges. In an industry defined by a “zero error” principle, hallucinations and opaque algorithms are unacceptable. Effective adoption demands transparency, human oversight, and rigorous safeguards. Even so, a new generation of AI startups is reimagining the accounting function, not just cutting costs, but uncovering insights and enabling strategic decision-making.

Part 1: State of the market

Whether it’s a two-person startup or a Fortune 500, accounting is the backbone of business that turns financial chaos into clarity, compliance, and confident decision-making. Traditionally built around a billable-hours model, the accounting profession includes hundreds of thousands of professionals across the US and Europe. In the US alone, there are more than 1.4 million accountants and auditors, and revenue of the US accounting services market has reached more than $145 billion (according to Statista) in 2025, with strong demand expected to continue.

Education pathways are also evolving, US firms like KPMG have historically required 150 credit hours to qualify for CPA licensing, but that model is being re-examined as fewer graduates enter the profession and as new skills – particularly in AI and ESG – are becoming essential. As the technological stack matures, accounting firms are poised for a major transformation driven by intelligent automation and data-centric innovation. To this end, (i) PwC is doubling down on AI investments, committing $1bn to scale AI capabilities across its audit and tax services or (ii) Thomson Reuters has acquired Materia, a specialist in agentic AI for the tax, audit and accounting profession.

However, AI is not synonymous with the idea that “the robots are coming for our jobs”. Indeed, the World Economic Forum predicts that AI and automation will create 58 million new jobs, mostly in high-skill roles. Historical parallels – like the rise of bookkeeping software in the 1980s – show that new technologies tend to transform, rather than eliminate, jobs. For example, despite fears, tools like Intuit and Excel led to a 75% growth in accounting roles over a decade, with workers taking on more complex tasks.

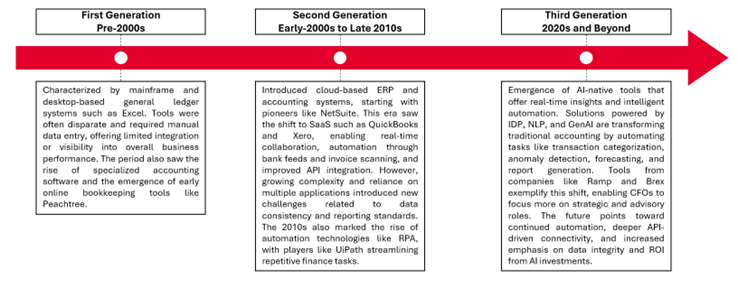

From the introduction of early bookkeeping software to today’s cloud-based platforms, accounting has gone through several major phases, each marked by significant advancements in tools and capabilities.

Part 2: AI’s role across the value chain

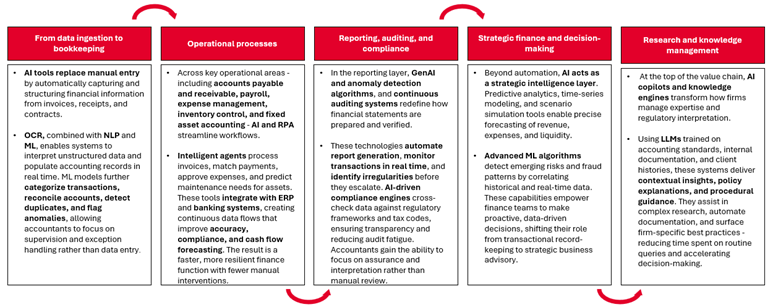

AI is rapidly transforming accounting end to end – automating routine work, improving accuracy, and unlocking real-time financial insight. From document processing to intelligent forecasting, these technologies are reshaping how finance teams operate:

- Intelligent Document Processing (IDP): Combines AI, OCR, and NLP to read, extract, and validate data from invoices, receipts, and contracts – cutting manual entry and improving tax and transaction accuracy.

- Chatbots & AI Agents: Manage queries, coordinate workflows, and generate reports – handling vendor questions, guiding staff through complex tasks, and streamlining financial research.

- Generative AI (GenAI): Produces reports, analyses, and contextual insights from large datasets – powering smarter AP/AR processes and faster, compliant reporting.

- Machine Learning (ML): Predicts trends, detects anomalies, and automates reconciliations – enabling better forecasting, fraud detection, and cost optimization.

- Robotic Process Automation (RPA): Executes repetitive workflows – such as payroll or reconciliations – while AI enhances accuracy and adaptive decision-making.

- Natural Language Processing (NLP) & Optical Character Recognition (OCR): Turn unstructured text and documents into structured data – extracting clauses, summarizing reports, and improving analytics.

Together, these technologies are turning accounting from a manual, backward-looking process into an intelligent, forward-looking engine of business insight. They collectively reshape the accounting value chain:

A key outcome of AI’s integration across the accounting value chain is the emergence of continuous closing – a model where financial data is captured, reconciled, and validated continuously rather than at month-end. By embedding automation and intelligence into daily workflows, accounting teams can maintain books that are always up to date, enabling real-time visibility into performance, liquidity, and compliance. This evolution eliminates the traditional “period-end crunch,” replacing it with ongoing accuracy and control. Machine learning and RPA reconcile transactions automatically, GenAI generates contextual reports on demand, and anomaly detection tools ensure integrity across systems. The result is a finance function that operates continuously, not retrospectively – one that delivers instant insights to support decision-making, strengthens governance, and underpins the shift toward an AI-native, real-time accounting environment.

Moreover, as automation takes over transactional work, the role of accountants is shifting from execution to strategic advisory and decision enablement. Instead of spending time on manual reconciliations, data entry, or compliance checks, finance professionals can focus on identifying and analyzing anomalies, interpreting insights, advising business leaders, and driving growth initiatives. AI copilots and intelligent assistants augment human expertise – suggesting optimizations, highlighting anomalies, and surfacing insights that guide strategic choices. This transformation elevates finance from a back-office function to a central intelligence hub that supports corporate strategy in real time. In this new paradigm, accountants become data interpreters, storytellers, and risk managers – bridging financial accuracy with business foresight. As a result, it appears that the winners in this transition will be firms that combine automation with human judgment, leveraging AI to amplify, rather than replace, financial expertise.

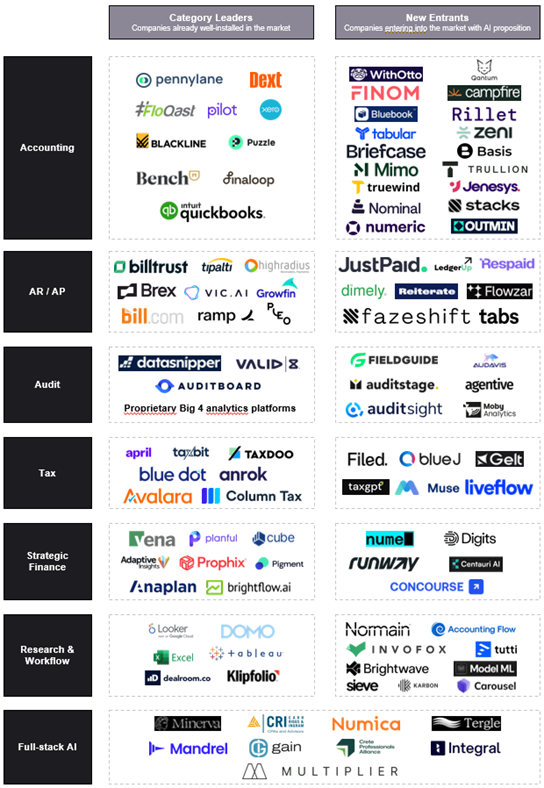

To conclude, the accounting technology landscape is rapidly evolving as AI reshapes every segment of the finance function. The market map below illustrates how the ecosystem is divided between established category leaders – firms that have built robust user bases and are integrating AI into mature platforms – and new entrants, which are introducing AI-first propositions to disrupt traditional workflows.

Part 3: Pathways to break in

- Product strategy: point solutions vs. full-stack AI platforms

The product strategy shaping AI adoption in accounting are mostly diverging into 2 models: AI agents and tools sold as B2B SaaS products and full-stack AI firms operating as automated accounting practices.

Source: The state of AI in accounting in 2025 by Karbon

The AI agent and tools model fits within the traditional enterprise software paradigm: vendors build systems to handle tasks like reconciliation, invoicing, tax filings, or anomaly detection, and license them to firms or finance teams. This SaaS motion – subscription-based, continuously updated, and workflow-integrated – is especially attractive to incumbents such as the Big Four, as it boosts productivity without disrupting client relationships or fee structures. Research already shows GenAI is “doing the boring stuff,” increasing reporting granularity and freeing accountants from repetitive tasks.

By contrast, full-stack AI companies seek to become the accountants themselves, offering end-to-end services in bookkeeping, payroll, reporting, and tax compliance directly to SMEs and individuals. These firms promise faster, cheaper delivery and higher margins by compressing labor into code. Some investors are backing the model: Y Combinator has encouraged “full-stack AI companies,” while Crete, backed by Thrive Capital, is deploying over US $500 million to consolidate practices. The TAM here extends far beyond software licenses to the full accounting revenue per customer. This playbook mirrors vertical SaaS but goes further by displacing incumbents entirely. Similar patterns are emerging in consulting, where Operand is building an AI-native firm rather than selling software. Yet execution risk is significant: full-stack ventures face licensing, liability, and operational complexity, as shown by Atrium’s failed attempt to become the “AI law firm of the future.”

For both models, the implication is clear: accountants themselves will need to evolve into something closer to data scientists, validating AI outputs and translating insights into business decisions. This is mirrored on the vendor side, where startups cannot succeed with engineers alone – they almost always need accountants embedded in their teams to encode domain expertise into scalable systems.

Ultimately, both models carry trade-offs. The agent approach is capital-light but risks commoditization as incumbents scale in-house tools. The full-stack path is more disruptive and economically expansive but also operationally demanding. Both are likely to coexist, at least in the beginning – with incumbents adopting agents to protect margins, while challengers pursue full-stack strategies to win market share. The competitive outcome will hinge on whether efficiency alone keeps clients loyal, or whether AI-native firms redefine what accounting services look like. This tension between point solutions and full-stack firms is also reflected in how vendors choose their target users.

2. Target users: empowering accountants vs. serving end customers

Just as product strategies diverge, go-to-market models also split serving accountants directly versus targeting SMBs directly. Each approach shapes product design, pricing, sales, and customer acquisition in different ways.

Companies like Pennylane or Karbon for example have built their go-to-market strategy around serving accountants as primary customers and distribution partners. Their platform is designed to facilitate collaboration with SME clients, with over 80% of customers acquired through accounting firms. This intermediary model creates a multiplier effect, as one accountant can bring dozens of SMEs, while also driving higher lifetime value through long-term client relationships. It further helps address complex regulatory requirements, since accountants already manage compliance across jurisdictions.

By contrast, other firms like Finom (an AVP portfolio company) adopt a direct B2B approach, targeting business owners with their Finom AI accounting platform made “by Entrepreneurs for Entrepreneurs”. Their platforms emphasize user-friendly interfaces, automation, and self-service, enabling companies to manage finances without professional expertise. These solutions rely on standardized pricing, online resources, and digital marketing to reach business owners at scale.

Ultimately, the choice between targeting accountants or businesses shapes product design, sales strategy, customer relationships, and regulatory compliance.

Part 4: Key risks & challenges

1.Reliability and accuracy

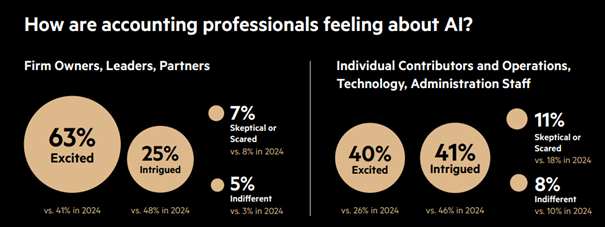

The implementation of AI in accounting is not without significant risks. The first and most immediate challenge is reliability. GenAI systems remain prone to hallucinations, model bias, and factual inconsistencies – issues that are unacceptable in a zero-tolerance compliance environment where even small errors can have regulatory or legal consequences. In parallel, the rise of deepfakes and synthetic data adds a reputational dimension: firms must prepare for the possibility that malicious actors could exploit AI for fraud or misinformation in financial records. This raises a fundamental question of accountability: if an error occurs, who bears ultimate responsibility – the accountant who relied on the AI tool, or the software provider who designed the system? In practice, regulatory frameworks still place the burden on licensed professionals, meaning accountants remain legally and ethically accountable for the accuracy of their work, even when assisted by AI. This creates additional pressure for firms to implement strong oversight, auditability, and governance mechanisms around AI adoption. It may also partially explain that while most accounting professionals are enthusiastic about AI, a portion remains intrigued yet cautious or even skeptical.

Moreover, most AI initiatives in accounting stumble at a critical juncture: the absence of contextual understanding. Current systems often process only summary-level data – trial balances, journal entries, or aggregated figures – without grasping the underlying transactions, attachments, and decision trails that shape financial outcomes. Yet it is precisely this context – who made a change, why a journal was adjusted, and how a discrepancy was resolved – that defines true accounting judgment.

Without this layer of understanding, AI models may generate statistically accurate yet operationally irrelevant insights. The next generation of AI-driven accounting platforms or AI agents must therefore evolve from data ingestion to context ingestion – learning from the complete history of financial activity to deliver insights that are not only correct but also explainable.

Ultimately, in accounting, real intelligence does not reside solely in data but in how professionals manage exceptions. Every manual correction, reclassification, or override embeds valuable information about context, policy, and intent. AI systems capable of capturing and learning from these micro-decisions can continuously refine their accuracy and adaptability.

Rather than viewing human oversight as a limitation, modern accounting platforms are redefining it as a feedback loop – transforming each human intervention into a data point that strengthens future automation. The result is a self-improving ecosystem where human expertise and machine learning co-evolve, driving both precision and trust.

2. Business model design

A second risk lies in the business model mismatch. Traditional accounting has long been structured around billable hours, with partners incentivized to maximize utilization. AI, by dramatically reducing the time required for routine tasks, threatens to cannibalize revenue in hourly billing departments such as tax.

While automation can improve margins in fixed-fee services like audit, vendors must carefully navigate these conflicting incentives. The SaaS subscription model – predictable, scalable, and volume-driven – clashes with legacy revenue structures, and it could create resistance to adoption inside firms.

3. Regulation hurdles and scalability

The accounting industry operates under stringent and often fragmented regulatory regimes that differ widely across jurisdictions. This contrast is especially clear when comparing Europe to the United States. In the US, firms operate within a highly unified framework: a single accounting standard (US GAAP), centralized oversight by the SEC and PCAOB, consistent audit requirements, and a nationally recognized CPA credential. This coherence enables providers to scale nationally with far fewer structural or regulatory barriers.

Europe presents a fundamentally different landscape. While listed companies apply IFRS, each of the 27 EU member states maintains its own local GAAP, professional licensing regimes, audit oversight authorities, tax codes, VAT structures, payroll systems, and statutory reporting rules. Even with EU-wide initiatives such as PSD2, Peppol, and ViDA, the practical realities of regulatory divergence remain. The result is a patchwork of obligations that varies significantly across borders – in sharp contrast to the unified US environment.

This structural difference is equally visible in market dynamics. Whereas the US supports a handful of large, truly national players capable of scaling uniformly across states, Europe’s leading incumbents – such as Visma, Sage, and Cegid – are in practice federations of regional products and localized acquisitions. Others, like Fortnox, Exact, and DATEV, succeed by staying deeply rooted in their domestic markets, where regulatory nuances and localized workflows create natural moats. In the US, a vendor can build once and distribute broadly; in Europe, successful players typically expand through adaptation, not uniformity.

For AI-driven accounting solutions, these regulatory differences translate into both technical and legal constraints. Model architectures, data pipelines, and compliance controls often require country-specific customization, particularly given Europe’s stronger emphasis on auditability, explainability, and data sovereignty. These requirements – while essential for trust – further widen the scalability gap between Europe and the US.

As a result, achieving pan-European scale remains significantly more complex than scaling within the United States. In the near term, AI entrants may find it more viable to target specific verticals, market segments, or national ecosystems, refining their models to align with local standards. Over time, regulatory harmonization or interoperable compliance frameworks could narrow the gap, but today, Europe’s regulatory diversity stands in stark contrast to the US’s unified system – and remains one of the most meaningful constraints for any AI solution seeking cross-border deployment.

4. Sales cycles

Compounding these issues are slow adoption cycles. Accounting firms are inherently risk-averse, operating with legacy systems and conservative IT budgets. Compliance committees and regulators tend to demand extensive validation before approving new workflows. While signals of modernization are emerging – PwC’s recent AI leadership hire and Sage’s partnership with AWS point to a shift – the pace remains gradual.

Despite these hurdles, several paths to mitigation are taking shape. New business models such as full-stack AI companies bypass the cannibalization problem by becoming the accounting firm themselves, monetizing efficiency rather than time. In parallel, the emergence of forensic AI startups – such as Valid 8, Resistant AI or Sedrant – provides safeguards against hallucinations, fraud, and data manipulation. Finally, the profession itself will adapt. Future accounting roles are likely to resemble hybrid positions that blend finance, data science, and engineering. Accountants will need to master data literacy, coding, and AI tools, while also strengthening communication skills to translate complex insights for clients and regulators.

Ultimately, AI in accounting remains in its early innings. The potential is clear, but widespread adoption will require addressing reliability, regulation, and business model alignment. Firms that prepare now – by cleaning data, experimenting with tools, and upskilling their teams – will be best positioned to thrive once AI reaches maturity.

Conclusion

The surge in recent fundraises across the accounting-technology sector signals a decisive shift in how investors – and increasingly the profession itself – view the future of finance operations. From large all-in-one platforms to highly specialized AI-native tools, capital is pouring into every layer of the accounting stack. In Europe, Pennylane’s €75 million round and Indy’s €40 million Series C underscore the strength of SME-focused suites, while enterprise challengers like Rillet, which raised US $70 million, are redefining what next-generation general-ledger infrastructure can look like. In the US, Maxima’s US $41 million fundraise highlights growing demand for AI solutions automating reconciliation and journal-entry workflows that legacy ERPs still treat as manual processes.

Beneath these headline rounds, the emergence of smaller, tightly focused startups illustrates how broad the innovation surface has become. Stacks has raised US $10 million to transform the financial-close process; Bluebook secured €3 million to push forward “self-driving accounting”; Briefcase raised €3 million to streamline SME bookkeeping and month-end workflows; Filed is expanding its compliance-automation capabilities with early-stage backing. Together, these companies reflect a market where both depth and specialization matter.

Yet despite this momentum, the path forward will be shaped by more than technology. Accounting is rooted in trust, rigor, and regulatory accountability. AI can revolutionize the discipline, but only if solutions are designed with the profession’s expectations in mind. This means moving beyond pure engineering toward a model where technical sophistication is paired with genuine accounting expertise. The industry’s evolution will hinge on teams that deeply understand not just automation, but the underlying logic of audit, tax, reporting, and judgment.

The future of accounting will therefore belong to hybrid organizations: engineers capable of pushing the boundaries of automation working alongside accountants who bring contextual understanding, compliance knowledge, and domain intuition. This pairing is already taking shape as firms hire data scientists next to CPAs and as startups embed accountants directly into product teams. The next era of accounting will not be defined by artificial intelligence alone, but by collaborative intelligence – where human expertise and technological innovation reinforce each other to build systems that are not only faster and smarter, but trustworthy and aligned with the realities of the profession.